Public Companies: Heartland Financial

KENT DARR Jan 10, 2018 | 3:56 pm

9 min read time

2,208 wordsBusiness Record Insider, Economic DevelopmentThe beginning and end of 2017 had a similar theme at Heartland Financial USA Inc., the Dubuque-based bank holding company that has sprawled over 12 states since its founding in 1981.

At the start of last year, Heartland was announcing the closing of one bank acquisition and an agreement to purchase another. At the end of the year, Heartland was closing another bank purchase and CEO Lynn “Butch” Fuller was in Lubbock, Texas, setting the stage for another acquisition.

Acquisitions — averaging almost two a year over the last five or six years, Fuller said — will push Heartland Financial above the $10 billion asset threshold this year, with no plans of stopping there.

Heartland traces its roots to the Great Depression and the formation of Dubuque Bank and Trust. Almost from the beginning, it was breaking the mold. Fuller’s grandfather, Lynn G. Fuller, helped negotiate a moratorium on farm mortgage foreclosures while working as a banker in Des Moines, prior to the formation of the Dubuque bank in 1935.

In 1981, when the Fuller family and other directors at Dubuque Bank and Trust formed Heartland Bancorp. — the predecessor of Heartland Financial USA Inc. — the city was noted for having the highest unemployment in the nation. The holding company was formed to enhance the bank’s chances for survival in a weak economy and provide the opportunity for increased equity for shareholders, all with the goal of going public and being listed on Nasdaq, Butch Fuller said.

With the ag economy faltering in the 1980s, Heartland decided to enter the ag lending market, targeting large operators who leadership figured would survive the recession.

A successful play, one that might have run counter to conventional thinking. “We’ve always been a bit of a contrarian,” Fuller said.

In 2003, after four years of being traded on the pink sheets, Heartland was listed on Nasdaq, where it has caught the attention of analysts who have been bullish on its earning potential and management style.

Fuller took some time recently to discuss Heartland’s business philosophy, its strategy for dealing with the extra regulatory challenges of being a $10 billion-plus operation, and its plans for the future. As for the future, the safe money would lead you to look at Heartland’s past.

First, give us a little background on the Fuller family’s history with Dubuque Bank and Trust and Heartland.

My grandfather was involved back in those early days, and eventually was the CEO, and then my father followed him, and I followed my father, and now my son is involved, here at the Dubuque Bank and Trust, as president and CEO. We just felt that, to be successful, we had to be uniquely different. [All of the Fullers who have led the banking operation share the same first name, Lynn.]

Back in 1981 when we formed the holding company, two objectives were in place. One was to get to a size where we could be listed on Nasdaq and have a publicly traded stock, so that the families that at one time had majority ownership of the stock, that were going to be passing that stock down through their estates — and knowing that the grandkids would be scattered all over the country — in order for them to feel good about the stock that they had, they would need to have some liquidity, because back in ’81, we didn’t have any liquidity. Basically, we had to trade the stock out of our desk drawer. If we didn’t have liquidity in the stock, those heirs to the stock would look at it and say, “Well, why don’t we just sell the company, because that’s the only way we can get a fair price.”

The goal was to get enough size to list on Nasdaq, and then beyond that, to maintain a unique difference in the industry. The unique difference, we felt, would be community banks. Yet, as time has gone on and the industry has consolidated, it became very clear that without scale, it was very hard to maintain a community bank approach.

Most of the banking companies of our size have collapsed their charters, but we have purposely not done that, because we still want to have the community bank touch. In the communities that we serve, we really feel that we have the big bank punch, meaning we have a very rich product line, far beyond what a community bank can offer because of our size and because of our technology and our talent. So, having that, but yet the right touch of a community bank, is a unique difference.

What are the ranges of services that you’re able to provide that the individual banks wouldn’t be able to provide if they were standing on their own?

Private client services would be one example. Private client services is wealth management, it’s retirement plans, it’s brokerage, retirement plans for companies. You got a whole suite of high-tech type of products for wealthy people and corporations that provide retirement plans for their employees. The technology cost there is very expensive. The talent cost is very expensive. The people that choose the investments and provide those investment alternatives and talk to the clients about their risk tolerance and fitting them into an appropriate investment, those are expensive people. Small banks that don’t have a lot of scale find it very difficult to provide those services.

Another area that is a challenge, and it has become more challenging as time has gone on, is residential real estate financing. When I started in the business back in the ’70s, I remember my first home loan, I signed four documents. Today, you sign 44 documents. The complexities of compliance and all of those things and the technology you need to hedge your pipelines and the servicing of those loans, it takes a lot of technology and a lot of talent. It’s very difficult for a small community bank to provide that type of structure. We have a $4 billion servicing portfolio. You need scale if you’re going to be able to afford the technology to manage that end of the business.

Commercial is a core part of our business, and treasury management has become a huge part of that. There again is very expensive technology. We’re trying to help our commercial clients save costs in their backroom. I mean, they can bank with us remotely online, they can open accounts online, they can see all of their transaction activity online. I think last year we invested probably over $5 million in primarily fraud protection type of software. The fraudsters get smarter every year, they work 24/7, so you’ve got to keep ahead of those guys. It’s critical that we protect our customers from those kinds of problems. Treasury management is a big part of it, fraud protection is a big part of it, and then you get over to the card services. We have a product called the purchase cards, so companies can use a credit card number to pay all of their payables and it’s automatically coming back onto their general ledgers in the appropriate accounts. That technology, to interface their payables, to automatically book into their general ledger after those items clear, is a huge cost savings for payables.

Then, beyond that, we will share some of the interchange income back with them. They actually have a cost savings in their backroom and then generate some new fee income that we’ll share back with them. Small community banks just don’t have these kinds of products and services, the technology and the talent it takes to deliver them.

That’s kind of a long ways away from where I started, but the idea back in 1981 was to get to a size where we can get our stock traded publicly, so we can treat our shareholders fairly, and let’s maintain a unique difference. The unique difference is this consortium of community banks, where Heartland, the holding company, provides the technology, the talent and the backroom for these banks, so the banks can really focus entirely on the customer.

Let’s talk about the future. Do you plan to veer away from acquisitions?

We generally have maybe 20 banks at any time that we’re talking to at some level. We’re in 12 states now. We have a lot of opportunities.

Did you ever feel the draw to set up shop in Greater Des Moines?

We’ve admired the Des Moines market, because it’s been a very growthy market for Iowa. The growth in Des Moines has been phenomenal. We just really never had the right fit to go in. We didn’t want to do a de novo into Des Moines, and we really didn’t have the right banking candidate to go into Des Moines with. We’ve had plenty of other opportunities to pursue. Some of these things just kind of work out, and sometimes they don’t. We wouldn’t be averse to going to Des Moines, but you have some pretty good banks in Des Moines.

What is your strategy for acquiring banks?

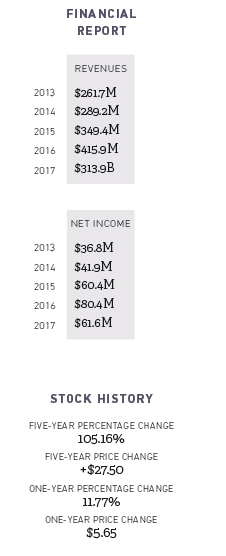

The combination of Signature Bank (in Minnesota) and First Bank and Trust in Lubbock will take us over $10 billion. Combined, that’s about $1.4 billion added on to our (current) $9.8 billion in assets. There’s another bank that we have that would be folding into one of our existing charters that’s about $500,000. So that $1.9 billion, plus organic growth, should take us by the end of ’18 to mid-’19 over $12 billion. After that, next stop would be $15 billion. So that’s kind of the way we think about it.

As far as our acquisition modeling, we run our own models. We don’t use an outside investment banker. There are really four things that are absolutely critical for any deal that we do.

First and foremost, it has to be accretive to our current shareholders’ earnings per share. Second, it has to give us an internal rate of return based upon very conservative estimates going forward of at least 15 percent. And many of these deals are up towards 20 percent or better. Third, we want an earn back on our premium, the goodwill piece; we want an earn back within four years. Preferably three, but if not, no more than four years.

And last, you have to have a good culture fit. If you don’t have a good culture fit, it’s very difficult to integrate the cultures of the companies.

How much time do you spend making that assessment?

I worked (with one bank) for 15 years before they decided that they wanted to call us and negotiate a transaction. And some of them it’s a matter of nine months. You just don’t know. We try to position ourselves with a lot of banks that when they decide it’s time to join somebody, we’re the first call they make. In many cases we can negotiate a transaction. First Bank and Trust Lubbock, that was a negotiated deal. We’ve been meeting with them for over two years. You just don’t know. It’s like fishing. You’ve got to have a lot of lines in the water.

You do have some specific challenges or regulatory burdens that you have to deal with when you become a $10 billion operation. How will you deal with those?

Here’s what we know is going to happen. We know that we’re going to lose our debit card interchange income. We think that’s somewhere around $5 million to $6 million pretax. The reason that we didn’t want to go over $10 billion in 2017 is because that’s when they measure your asset size. They do it at the end of the calendar year. So as long as we remained below $10 billion through ’17, the next measurement period will be Dec. 31, 2018. Then you have six months thereafter before you start to lose your interchange income. So we’re out to mid-2019 before that interchange income starts to dissipate. That’s why we want to be at $12 billion in total assets. That additional $2 billion of earning assets will easily cover a lot of that loss. So the loss of that $5 million or so will be mitigated considerably because we’ll have a much larger earnings base by then. That was the plan.

Are there any challenges you see ahead? Any gray clouds?

We’ve been in the recovery for a very long time now. Most recoveries, if they go nine, 10 years, that’s a long time. So you always wonder when we’re going to start going off the other side. Now there’s a lot of optimism in the market with the opportunity for federal tax reductions, regulatory relief, so forth and so on. You’ve seen bank stocks rally considerably because of those things. So in the short run, things look pretty positive. But you know, what goes up will come down eventually, so you always wonder when the next recession is going to hit. … In general the biggest challenge I see is always being able to attract and retain the kind of talent you need to continue to grow a company like ours. Your company is only as good as your people. So finding talent is always the biggest challenge.

Trending News