How to Avoid Tyrannically Urgent Yet Unimportant Investment Ideas

Business Record Staff May 24, 2021 | 9:44 pm

6 min read time

1,420 wordsBusiness Insights Blog, Finance

BY KENT KRAMER, CFP®, AIF®, Foster Group

Every week it seems there is a new story about which investment, which “trade,” is making amazing money. From the FANMAG stocks, to Tesla, GameStop, and Crypto, each new headline appears important and creates feelings of urgency to those paying attention.

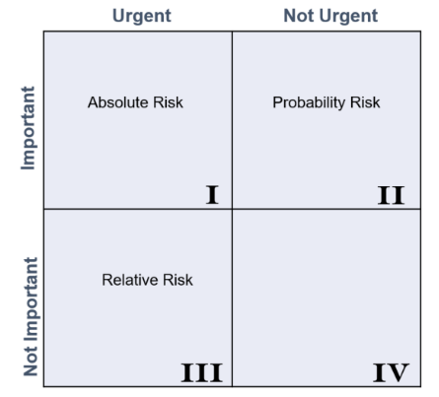

I confess that I love time management books. Steven Covey, writing with Roger & Rebecca Merrill (the “Merrills”), published First Things First in 1994. The key idea of their book is something called Quadrant II time management1, the conscious prioritization of the important but not urgent things. I have found the grid they developed for evaluating the uses of time can also be very helpful in identifying and evaluating three types of investment risk as well:

- Absolute Risk is related to the question, “How much can I lose?”

- Probability Risk addresses the question, “What is the probability of not reaching my goal?”

- Relative Risk asks, “How much more (or less) could I make than my ‘benchmark,’ or whatever I am comparing to?”

Of these three risks, which one seems the most important to you as an investor? Which one seems to be the most urgent? As we’ll see, each of these are real risks, because if they are unmanaged or unanticipated, they may cause investors to focus on the wrong things at the wrong times and lead to actions that may sabotage goals and portfolios.

Quadrant I: Urgent & Important

In the case of a market crisis (think “Bear Market”), Quadrant I decisions, things that are urgent and important, come into play. For most investors, Absolute Risk and the associated Fear of Loss, lives here. Absolute Risk is important because big losses can be very hard to recover from and going to zero may be unrecoverable. Also, in rapidly falling markets, there is a risk of selling at the wrong time, either because of our Fear of Loss or because we have a need for cash that we did not plan for.

Quadrant III: Urgent & Not Important

In Quadrant III, Relative Risk takes things that feel urgent and fools us into thinking these things are also important. “FOMO,” the Fear of Missing Out, lives here. Covey and the Merrills named Quadrant III the “Quadrant of Deception.” Anyone who has wondered if they really missed the opportunity of a lifetime by not investing heavily in Tesla, GameStop, or Bitcoin understands what FOMO can feel like. Even though virtually no one’s portfolio is competing with Bitcoin’s past 12 month return of more than 360% (as of May 18, 2021),2 we still think “what if I had done that?”

In a similar way, investors may be tempted to compare their diversified portfolio returns to what they hear “the market” is doing lately. Often “the market” in the news is a very small portion of the true global market. US newscasts tend to report on the 30 companies in the Dow Jones Industrials or one of the 6 big tech firms in FANMAG when the global stock market consists of more than 45,000 listed companies.

We may experience the downside of Relative Risk by comparing our portfolio’s return to an unrealistic benchmark. Taking action in response to that disappointing comparison may then feel urgent and important if we don’t have a clear idea of what long-term rates of return are required for helping achieve our goals, along with what kinds of protection we need from catastrophic risk. Urgently chasing short-term returns, as in the case of people investing in Bitcoin in late 2017 and GameStop in late February of this year, can lead to disappointing results. The deception of this quadrant is the temptation to think that something is both urgent and important when really it only feels urgent and is not important to accomplishing the things that matter most.

Quadrant II: Important but Not Urgent

For long-term success, the planning and preparation associated with managing Probability Risk ends up in Quadrant II, vitally important but often not urgent. We may all recognize how important good planning and preparation are, but usually there are no news headlines screaming at us to address our long-term plans RIGHT NOW!

The goals associated with managing Probability Risk in our financial planning and investing include clearly understanding our financial goals, knowing what rates of return are required to help achieve them, and taking protective steps to help minimize downside risks. In this quadrant, we focus on creating the highest probabilities of success.

For example, what if your goals require a 7% annualized return and you can get that, or something close to it, with 85% certainty in a portfolio that also limits large and permanent losses? Knowing that, why would you risk significant dollars on an investment that could return 1000% but may have a greater than 50% chance of going to zero?

Warren Buffett has summed up this idea well, saying many times, “…it is insane to risk what you have and need in order to obtain what you don’t need.”

If we do a good job of addressing Probability Risk in Quadrant II, by extension we will have taken many positive steps in managing Absolute and Relative Risk, as well. We will have taken great care to define what our key benchmarks for success should be. These will include knowing what long-term rate return we need to help achieve our financial goals, what amount of the portfolio needs to be insulated from stock market risk, and how much we need to save and invest each year in order to provide us with the highest probability of success. Then, when Bear Markets ultimately arrive, we already will have prepared for them with protective cash reserves and diversification. And when the next GameStop frenzy emerges, we can rest assured, knowing that the enticingly possible but highly improbable returns we are hearing about are not needed for our success. We can avoid the traps of wrongly understood Relative Risk that exist in the Quadrant of Deception!

Charles Hummel penned Tyranny of the Urgent in 1967. His insights about letting feelings of urgency keep us from attending to more important matters, are as relevant today as they were then. The words in parenthesis are my application of his thoughts to our consideration of investment risks.

“…the momentary appeal of these tasks (paying attention to urgent yet unimportant risks) seems irresistible and important, and they devour our energy. But in light of time’s perspective, their deceptive prominence fades; with a sense of loss, we recall the vital tasks (of attending to not urgent yet vitally important risks) we pushed aside. We realize we’ve become slaves to the tyranny of the urgent.”3

1 Steven Covey, A. Roger and Rebecca R. Merrill, First Things First, Simon & Schuster, 1994

2 Source: Y Charts, NYSE Bitcoin Index

3 Charles E. Hummel, Tyranny of the Urgent, InterVarsity Press, 1967

PLEASE SEE IMPORTANT DISCLOSURE INFORMATION at www.fostergrp.com/disclosures. A copy of our written disclosure Brochure as set forth on Part 2A of Form ADV is available at www.adviserinfo.sec.gov. Past performance does not guarantee future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment or investment strategy (including those undertaken or recommended by Foster Group), will be profitable or equal any historical performance level. All investment strategies have the potential for profit or loss. Investment strategies such as asset allocation, diversification, and rebalancing do not assure or guarantee better performance and cannot eliminate the risk of investment losses. There is no guarantee that a portfolio employing these or any other strategy will outperform a portfolio that does not engage in such strategies. Any projections in this article is not a prediction or projection of actual investment results and there can be no assurance that any projection will be achieved. Changes in investment strategies, contributions or withdrawals may materially alter the performance of an individual’s portfolio. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there are no assurances that it will match or outperform any particular benchmark. Projections, forecasts and estimates referenced on the Website are not purely historical in nature and are therefore necessarily speculative and subject to material variation. Kent Kramer, CFP®, AIF®, is a registered investment adviser representative of Foster Group, Inc., an investment adviser registered with the U.S. Securities Exchange Commission since 1991.

|

Kent Kramer View Bio |

Trending News